- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Bill Splitting Apps Market Size & Forecast 2025–2034 | 8.4% CAGR

Global Bill Splitting Apps Market Size, Share & Strategic Growth Analysis – By Platform (iOS, Android, Web-Based), By Deployment (Cloud-Based, On-Premises), By Application (Peer-to-Peer Payments, Group Travel, Roommate Expense Sharing, Corporate Expense Management), By End-User (Individuals, SMEs, Enterprises), By Region, Competitive Landscape, Digital Payment Trends, Investment Insights & Forecast 2025–2034

Report Overview

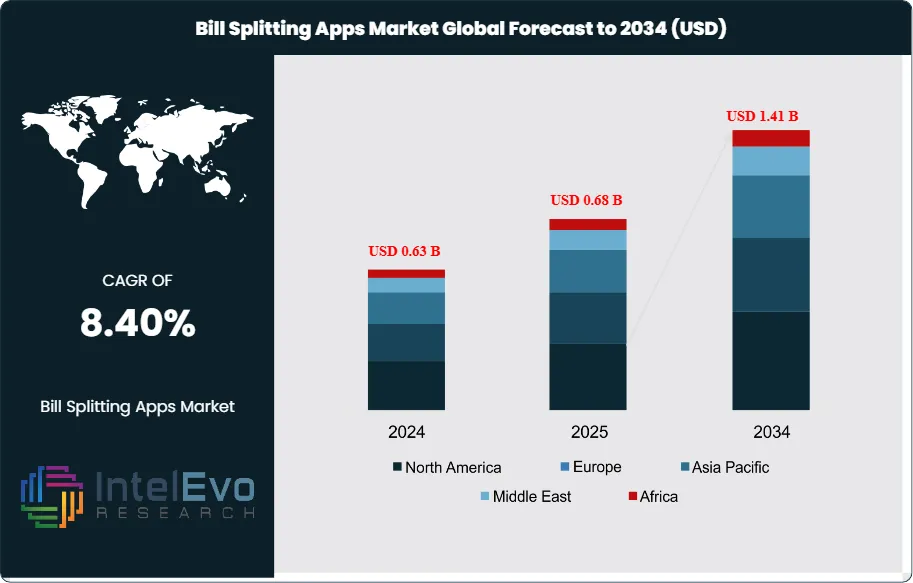

The Global Bill Splitting Apps Market was valued at approximately USD 0.63 billion in 2024 and is projected to reach nearly USD 1.41 billion by 2034, driven by increasing digital payment adoption, peer-to-peer transaction growth, and the rising popularity of shared economy platforms. Based on the established growth trajectory, the market size for 2025 is estimated at approximately USD 0.68 billion. From 2026 onward, the market is expected to expand at a compound annual growth rate (CAGR) of approximately 8.4% during 2026–2034, ultimately reaching around USD 1.41 billion by 2034.

Get More Information about this report -

Request Free Sample ReportBill splitting applications enable consumers to divide shared expenses, record who owes what, and settle payments in real time. They run on major mobile operating systems and cover use cases from household utilities and rent to restaurants, groceries, and group travel. Rising smartphone penetration, wider access to digital payments, and growing use of peer-to-peer (P2P) platforms form the core demand engine.

Consumer adoption data reinforces this shift. A recent survey of 1,000 U.S. adults using P2P platforms such as Venmo, Zelle, PayPal, and Cash App shows that 47% split everyday expenses through these channels. Usage is strongest among younger cohorts: about 60% of adults aged 18–25 and 58% of those aged 26–41 use these tools at least weekly to share costs. Inflation and pressure on disposable incomes accelerate this behavior, with more than half of younger users reporting that rising prices have increased their reliance on payment apps to manage shared outlays.

On the supply side, competition increases as fintechs, banks, and super-apps embed bill sharing functions into broader payment ecosystems. Vendors invest in artificial intelligence and machine learning to automate receipt capture, categorize spending, recommend fair splits, and surface insights on spending patterns. Automation reduces friction in settlement, while experiments with blockchain seek to improve transaction security, auditability, and trust in multi-party records.

Regulation and risk shape market strategy. Data privacy laws, payment security standards, and know-your-customer and anti-money-laundering obligations raise compliance complexity, especially for cross-border transfers. Cybersecurity threats and fraud risk demand sustained investment. Revenue models that depend on interchange fees and merchant commissions face possible pressure from fee caps and evolving payment rules.

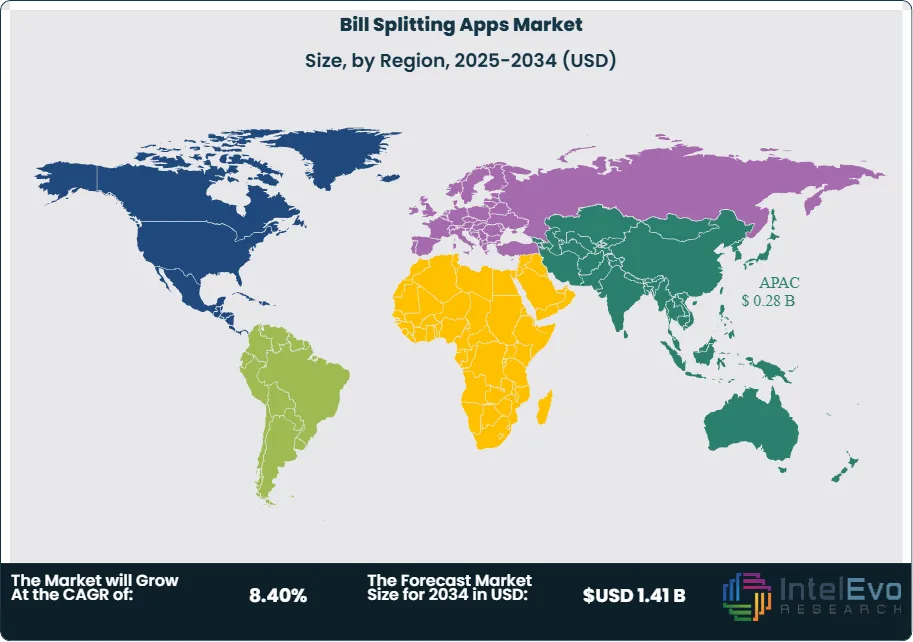

Regionally, Asia-Pacific represents the largest opportunity pool. In 2024, the region is estimated to generate about USD 0.26 billion in revenue, or roughly 41% of global spend, supported by mobile-first consumers and expansion in digital wallets and super-apps. North America and Europe remain regulation-intensive markets anchored in P2P payment networks, while Latin America and the Middle East and Africa are emerging as fast-growth hotspots as financial inclusion and smartphone adoption advance.

, By Deployment (Cloud-Based, On-Premises), By Application (Peer-to-Peer Payments, Group Travel, Roommate Expense Sharing, Corporate Expense Management), By End-User (Individuals, SMEs, Enterprises), By Region, Competitive Landscape, Digital Payment Trends, Investment Insights & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global bill-splitting apps market stood at 0.58 billion USD, 2023 and is on track to reach estimated: 1.41 billion USD, 2034, reflecting an estimated: 8.4% CAGR, 2024-2034. This trajectory implies an intermediate market value of estimated: 0.63 billion USD, 2024 as adoption continues to scale.

- Segment Dominance: Android-based applications held a 58.0% share, 2023, supported by affordable devices and wide app store reach. This segment is likely to maintain a lead with an estimated: 60.0% share, 2034 as emerging markets keep favoring Android ecosystems.

- Segment Dominance: Private users accounted for a 75.0% share, 2023, reflecting strong use among friends, families, and small social circles. This customer group is projected to sustain an estimated: 72.0% share, 2034 as social expense management remains the primary use case.

- Driver: Rising smartphone and digital payment adoption, especially among millennials and Gen Z, underpins demand, with estimated: 75.0% smartphone penetration, 2024 in key urban markets. Increasing frequency of shared spending events, such as dining and travel, further accelerates transaction volumes toward an estimated: 2.0 billion app-facilitated splits, 2030.

- Restraint: Data privacy concerns and uneven regulatory frameworks in payments and data protection can slow user onboarding, particularly in mature markets, where an estimated: 30.0% of the user base, 2024 remains cautious about sharing financial details. Compliance costs linked to KYC and AML requirements may lift operating expenses by an estimated: 10.0% per provider, 2025.

- Opportunity: Vendors can expand revenue by integrating advanced budgeting, analytics, and cross-border payment features, targeting an estimated: 40.0% of users, 2026 seeking richer financial tools. Partnership-driven models with banks, merchants, and travel platforms could unlock incremental transaction revenue of estimated: 0.25 billion USD, 2030.

- Trend: Platforms increasingly embed AI and automation to categorize expenses, recommend splits, and detect anomalies, with an estimated: 55.0% of leading apps, 2027 offering AI-powered features. Integration with P2P payment rails and digital wallets is expected to support an estimated: 65.0% of in-app settlements, 2030.

- Regional Analysis: APAC led the market with over a 41.0% share, 2023, driven by a tech-aware population and expanding internet and wallet usage. The region is expected to reach estimated: 44.0% share, 2034, while North America and Europe together contribute an estimated: 38.0% share, 2034 under more mature regulatory regimes.

By Platform

Android continues to hold the largest share of the bill splitting apps market in 2025 as global Android penetration remains above 70 percent. The platform benefits from its presence across a wide range of price tiers, which makes digital financial tools accessible to high-income and budget-conscious users alike. This reach is particularly important in mobile-first regions such as India, Southeast Asia, and parts of Africa, where Android accounts for the majority of smartphone shipments and where app adoption directly follows device availability. As bill splitting apps scale into emerging markets, Android’s embedded base offers clear volume advantages.

The segment’s growth is supported by Android’s open development environment. Developers can integrate APIs from payment gateways, banking networks, and identity verification systems with fewer restrictions. This supports faster deployment of features such as NFC-based payments, biometric authentication, and real-time settlement. These capabilities help providers serve users who want faster calculations, automated reminders, and immediate reconciliation across peer groups. iOS maintains strength in North America and parts of Western Europe where higher-end device use remains consistent, but Android retains leadership in global transaction volume due to its much larger installed base.

Looking beyond 2025, platform competition will revolve around the depth of financial integrations. Android’s flexibility positions it well to absorb new compliance requirements and support advanced features such as AI-driven analytics and multi-currency handling. These advantages are expected to reinforce Android’s leadership as bill splitting tools expand into broader personal finance ecosystems.

By End-User

Private users continue to form the core of demand in 2025, accounting for an estimated three-quarters of total app activity worldwide. Adoption is strongest among younger demographics that rely on mobile payments for dining, travel, rent sharing, and recurring household expenses. Rising smartphone access and consistent growth in digital payment volumes support this segment. India alone processed more than 18,000 crore digital transactions in FY 2023–24, and similar momentum is visible across Southeast Asia and Latin America. These conditions give private users strong incentives to adopt tools that simplify shared spending and reduce manual calculation errors.

Commercial users represent a smaller but expanding portion of the market. Small teams, freelancers, and shared workspace communities are adopting bill splitting platforms to manage pooled resources and track expenses across projects. Integration with accounting software and automated recordkeeping positions these apps as lightweight financial management tools for microbusinesses. As companies expand remote-work models, the need for transparent shared spending tools grows, especially in industries with distributed teams and frequent operational reimbursements.

Across both segments, technology adoption shapes the competitive landscape. Providers are integrating AI to improve receipt extraction, recommend splits, and predict recurring transactions. These features reduce user effort and increase engagement, which supports market expansion through 2025.

By Application

Bill splitting apps are used primarily for shared personal and household expenses, which represent the largest application area in 2025. Dining, entertainment, rent sharing, and group travel account for the majority of transaction volume. These categories benefit from high-frequency usage patterns and the rapid shift to cashless payments. Apps that support instant settlement, multi-user approvals, and cross-border exchanges capture higher retention rates.

Group-based financial management is expanding as users adopt apps for event planning, shared memberships, and community-based contributions. This includes subscription sharing, charity pooling, and joint purchases. These emerging applications show rising appeal in regions where digital wallets are widely used. As third-party integrations deepen, app providers can support automated bill imports from merchants, which reduces manual entry and increases accuracy.

Enterprise-linked applications remain smaller but show growing demand. Teams use shared expense tools for travel coordination, departmental outings, and collaborative purchases. As companies seek transparency in small recurring costs, adoption of app-based tracking continues to increase, especially within SMEs.

By Region

Asia Pacific leads the bill splitting apps market in 2025, supported by high smartphone penetration and rapid adoption of mobile payment systems. Markets such as India, Indonesia, and Vietnam continue to drive digital transaction growth, creating strong demand for peer-based financial tools. Android’s dominance in this region amplifies uptake. Many global and regional app providers focus their expansion strategies here due to the scale of addressable users.

North America maintains strong revenue contributions due to high adoption of platforms like Venmo, Cash App, and Splitwise. User expectations center on seamless integration with banking systems and real-time P2P transfers. Europe follows with steady adoption driven by regulated digital payment frameworks and the growing popularity of group travel and subscription sharing. Markets such as the UK, Germany, and France show increasing activity among private users and small teams that prefer simple expense management tools.

Latin America and the Middle East and Africa are emerging growth zones. Rising smartphone access and the expansion of regional digital wallets create favorable conditions for bill splitting applications. Providers that localize interfaces and integrate regional payment methods are likely to gain early advantage. As consumer trust in app-based finance strengthens, these regions present long-term growth potential through 2030.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Platform

- iOS

- Android

By End-User

- Private Users

- Commercial Users

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 0.68 B |

| Forecast Revenue (2034) | USD 1.41 B |

| CAGR (2025-2034) | 8.40% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Platform (iOS, Android), By End-User (Private Users, Commercial Users) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Splitwise Inc., Groupee Pty Ltd., NBK, Splid, DigiGround Pty Ltd., Paerpay Inc., Kittysplit UG, ApTap Ltd., Bill.com LLC, MWYN Tech Pvt. Ltd., Axio Digital Pvt. Ltd., Block Inc., Splittr, NatWest Group Plc, Step Up Labs Inc., PayPal Holdings Inc., Tricount S.A., Standy Software, Microsoft Corp., bring10 LLC, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Cloud-Based, On-Premises), By Application (Peer-to-Peer Payments, Group Travel, Roommate Expense Sharing, Corporate Expense Management), By End-User (Individuals, SMEs, Enterprises), By Region, Competitive Landscape, Digital Payment Trends, Investment Insights & Forecast 2025–2034")

, By Deployment (Cloud-Based, On-Premises), By Application (Peer-to-Peer Payments, Group Travel, Roommate Expense Sharing, Corporate Expense Management), By End-User (Individuals, SMEs, Enterprises), By Region, Competitive Landscape, Digital Payment Trends, Investment Insights & Forecast 2025–2034")

, By Deployment (Cloud-Based, On-Premises), By Application (Peer-to-Peer Payments, Group Travel, Roommate Expense Sharing, Corporate Expense Management), By End-User (Individuals, SMEs, Enterprises), By Region, Competitive Landscape, Digital Payment Trends, Investment Insights & Forecast 2025–2034")

Frequently Asked Questions

How big is the Bill Splitting Apps Market?

Global Bill Splitting Apps Market valued at USD 0.63B in 2024, projected to reach USD 1.41B by 2034 at 8.4% CAGR, driven by digital payments and P2P transaction growth.

Who are the major players in the Bill Splitting Apps Market?

Splitwise Inc., Groupee Pty Ltd., NBK, Splid, DigiGround Pty Ltd., Paerpay Inc., Kittysplit UG, ApTap Ltd., Bill.com LLC, MWYN Tech Pvt. Ltd., Axio Digital Pvt. Ltd., Block Inc., Splittr, NatWest Group Plc, Step Up Labs Inc., PayPal Holdings Inc., Tricount S.A., Standy Software, Microsoft Corp., bring10 LLC, Other Key Players

Which segments covered the Bill Splitting Apps Market?

By Platform (iOS, Android), By End-User (Private Users, Commercial Users)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date